Many people think using multiple crypto exchanges is just a smart way to get around limits-like trading when one platform is down, or accessing coins not available in their country. But what they don’t realize is that this practice is often a red flag for regulators, and in many cases, it’s directly tied to illegal activity. If you’re hopping between exchanges to bypass rules, you’re not just being clever-you’re playing with fire.

How People Try to Avoid Restrictions

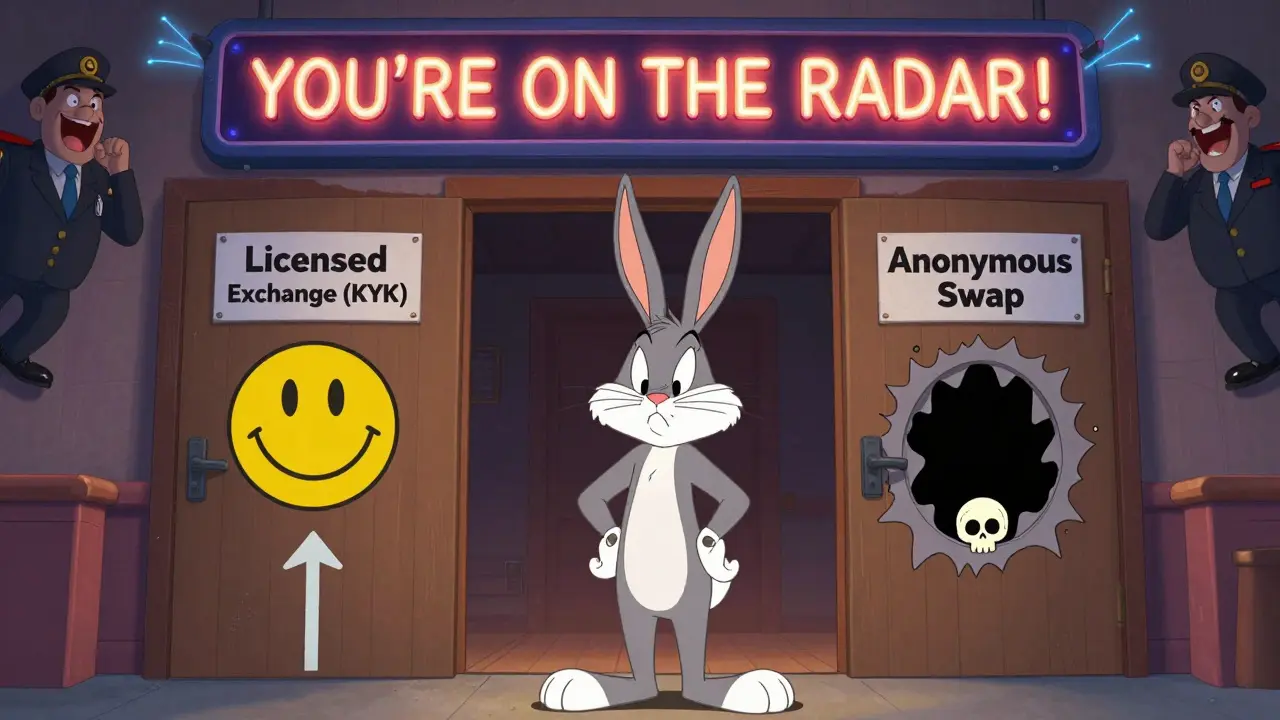

The most common way users try to dodge restrictions is by using nested exchanges. A nested exchange is a platform that doesn’t hold your crypto directly but instead uses accounts on other exchanges to trade on your behalf. Think of it like a middleman who takes your money, then goes to another exchange to buy Bitcoin for you. Sounds harmless, right? Not always.These platforms often skip Know Your Customer (KYC) checks. That means no ID, no proof of address, no questions asked. Some even advertise themselves as "no KYC" or "anonymous trading". That’s not convenience-it’s a warning sign. Legitimate exchanges take days to verify you. If a platform lets you trade instantly with no paperwork, it’s likely designed for evasion.

Another method is using decentralized exchanges (DEXs). Unlike centralized platforms, DEXs run on smart contracts and don’t have a company behind them that can be shut down. Because there’s no central authority, governments can’t force them to freeze accounts or report users. This makes them popular among criminals looking to move funds without leaving a paper trail.

Then there are non-compliant exchanges. These are platforms based in countries with weak or no enforcement of sanctions, like Russia, North Korea, or certain jurisdictions in Eastern Europe. Criminals specifically target these because they know they won’t be asked where their money came from. Some even openly boast about helping users bypass U.S. or EU sanctions.

What Happens When You Cross the Line

In March 2025, the U.S. Treasury’s Office of Foreign Assets Control (OFAC) took down Grinex. Grinex wasn’t some shady startup-it was created by the same team behind Garantex, a major exchange that had just been sanctioned. Their entire purpose? To keep moving money after Garantex got frozen. Grinex’s own website said it was "built to support users affected by sanctions." Within months, it handled billions in transactions.That’s not an outlier. It’s a blueprint. When one exchange gets shut down, bad actors simply launch another one with a new name. They reuse old customer lists, steal verified accounts, and reroute funds through layers of wallets and exchanges. The goal? To make it impossible to trace where the money started.

And it’s not just about sanctions. The SEC has made it clear: if a platform brings together buyers and sellers using fixed rules, it’s operating like an exchange-and it must register. Many platforms claiming to be "wallets" or "peer-to-peer services" are actually unregistered exchanges. If you trade on them, you’re participating in an illegal operation.

The Hidden Dangers for Users

Using multiple exchanges sounds like a way to stay safe, but it often does the opposite. When you use a nested exchange, you’re giving them full control over your funds. They hold the private keys. They can freeze your assets. They can disappear overnight. And if they’re involved in laundering, your account could get flagged-even if you didn’t know what they were doing.Cybercriminals exploit this. They steal login details from legitimate users, then use those verified accounts on compliant exchanges to move illicit funds. If you’re the source of those funds-even unknowingly-you could be dragged into an investigation. Law enforcement doesn’t care if you were "just trading." If your wallet sent money to a sanctioned address, you’re a target.

Even simple tools like coin swap services. These are chat-based platforms where you trade crypto for cash or other coins without signing up. They’re marketed as "fast" and "easy," but they’re perfect for ransomware gangs and drug dealers. There’s no history, no trace, no accountability.

How Regulators Are Fighting Back

Regulators aren’t sitting still. The U.S. Treasury now requires all virtual currency firms to implement strict internal controls:- Screening every transaction against sanctions lists

- Monitoring for "red flags"-like sudden large transfers, multiple small deposits from different sources, or rapid movement between exchanges

- Keeping detailed records for at least five years

- Reporting suspicious activity to financial authorities

Tools like blockchain analytics software can now track money across dozens of wallets and exchanges. If your crypto moves from a sanctioned wallet, through a DEX, into a nested exchange, then out to a mainstream platform, regulators can still trace it. It just takes time-and they have that time.

One of the most concerning trends is the rise of sanctioned tokens. For example, A7A5-a digital asset backed by the Russian ruble-was created specifically to bypass Western financial controls. It’s traded on non-compliant exchanges and used to buy goods, services, and even weapons. This isn’t science fiction. It’s happening now.

Legitimate Reasons vs. Illicit Use

Not everyone using multiple exchanges is breaking the law. Some traders use them for legitimate reasons:- Arbitrage: buying Bitcoin cheaper on one exchange and selling it higher on another

- Liquidity: accessing tokens not listed on their home exchange

- Backup: having funds on multiple platforms to avoid downtime

But here’s the line: if you’re doing any of those things while avoiding KYC, hiding your identity, or using platforms that don’t report activity-you’re crossing into risky territory. Regulators don’t care if you think you’re being smart. If your actions match the pattern of evasion, you’re on their radar.

What You Should Do Instead

If you’re worried about restrictions, here’s what actually works:- Use only licensed, regulated exchanges with clear KYC policies

- Don’t use platforms that promise "no verification"-they’re not protecting you, they’re exposing you

- Keep all your transactions on one or two trusted platforms

- If you need to move funds internationally, use bank transfers or licensed remittance services, not crypto

- Always check if an exchange is on OFAC’s sanctions list

There’s no shortcut to safety. Trying to outsmart the system with multiple exchanges doesn’t give you freedom-it gives you risk.

Final Warning

The days of anonymous crypto trading are ending. Governments are coordinating. Tools are getting smarter. And the penalties? They’re severe. Fines can reach millions. Accounts get frozen. In some countries, you could face jail time.If you’re using multiple exchanges to avoid restrictions, ask yourself: Are you trading for profit-or are you playing a game where the rules keep changing, and the house always wins?

Is it illegal to use multiple crypto exchanges?

It’s not illegal to use more than one exchange. But if you’re using them to bypass sanctions, avoid KYC checks, or hide the source of funds, then yes-you’re breaking the law. Regulators look at behavior, not just the number of platforms you use.

Can I get in trouble if I didn’t know a platform was sanctioned?

Ignorance isn’t always a defense. If you used a platform that was publicly listed as sanctioned by OFAC or another authority, and you didn’t check, you could still face penalties. Always verify an exchange’s compliance status before depositing funds.

What’s the difference between a nested exchange and a regular one?

A regular exchange holds your crypto and trades directly on its own system. A nested exchange doesn’t hold your assets-it uses accounts on other exchanges to trade for you. This adds a layer of secrecy, which is why it’s often used for evasion. You don’t control the keys, and you can’t track exactly where your money goes.

Are decentralized exchanges (DEXs) safe to use?

DEXs are technically safe if you’re trading your own funds and know what you’re doing. But they’re also the go-to tool for criminals because there’s no KYC, no reporting, and no way to freeze accounts. If you’re using a DEX to move money quickly without questions, you’re likely enabling illegal activity-even if you don’t realize it.

How do regulators track crypto across multiple exchanges?

Blockchain analysis firms use tools that trace every transaction across wallets, exchanges, and DEXs. Even if money moves through 10 different platforms, they can follow the trail using patterns, timestamps, and wallet connections. It’s not magic-it’s math. And it works.

What should I do if I’ve already used a non-compliant exchange?

Stop using it immediately. Withdraw any remaining funds to a regulated exchange where you’ve completed KYC. Keep records of all transactions. If you’re concerned about past activity, consult a legal professional who specializes in crypto compliance. Don’t wait for a notice from regulators.

Oh wow, finally someone says it out loud. I’ve seen so many people bragging about how they ‘outsmarted the system’ using nested exchanges-like it’s some kind of hack. Newsflash: you’re not a genius, you’re a walking target. Regulators don’t care if you ‘didn’t know’-they see the pattern, and patterns get flagged. I had a friend get audited because she used a ‘no-KYC’ platform to swap ETH for USDT. Turns out, the platform was laundering money for a ransomware group. She didn’t touch illegal coins, but her wallet was linked. Now she’s got lawyers. Don’t be her.

Also-why do people still think DEXs are ‘safe’? They’re not. They’re just invisible. And invisible doesn’t mean untraceable. It means the trail is longer, and when they catch you, it’s worse.

Stop romanticizing anonymity. It’s not freedom. It’s a trap dressed up as a loophole.

Interesting how we’ve turned financial sovereignty into a game of whack-a-mole with regulators. 🤔

There’s a deeper philosophical tension here: the individual’s right to self-sovereignty vs. the state’s need for control. Crypto was supposed to be the great equalizer-until everyone started using it to dodge taxes, sanctions, and KYC like it was a video game cheat code.

Let’s not pretend the system is pure. Banks launder billions daily. But when a guy in Ohio uses Binance and KuCoin to arbitrage BTC? Suddenly he’s a criminal. Double standards, anyone?

Maybe the real issue isn’t the users-it’s the hypocrisy of a system that demands compliance while refusing transparency.

Just saying. 🙃

I find it profoundly disturbing that people still treat crypto as if it’s a frontier where rules don’t apply. This isn’t the Wild West. It’s a regulated financial ecosystem with forensic tools that can trace a single satoshi across 27 wallets. The fact that anyone still believes they’re ‘hiding’ is not just naive-it’s dangerous.

And yet, here we are. People risking their homes, their careers, their freedom because they watched a YouTube video titled ‘How to Trade Crypto Anonymously (Legally!)’.

There’s no such thing as anonymous crypto anymore. If you think there is, you’re not clever. You’re a liability.

My cousin got flagged because he used a non-KYC exchange to buy Solana. He thought it was ‘just a small trade’. Turns out, the wallet he bought from was linked to a North Korean hacking group. Now he’s on OFAC’s watchlist. He didn’t know. He didn’t mean to. But guess what? They froze his bank account. Took 8 months to prove he wasn’t a criminal. He lost his job. His credit is ruined. He’s 24. This isn’t a warning-it’s a death sentence for the unprepared.

Stop being cool. Start being careful.

man i just wanna buy some dogecoin and chill why does everything have to be so complicated now? i dont even know what a nested exchange is but i heard its good for ‘liquidity’ so i used it. now im scared to touch my wallet. lmao

You’re all missing the point. This isn’t about legality. It’s about power. The state doesn’t care if you’re breaking rules-it cares if you’re bypassing its control. The moment crypto became decentralized, the elites panicked. Now they’re weaponizing compliance to force everyone back into the system. That’s why they’re targeting nested exchanges, DEXs, and ‘anonymous’ swaps. Not because they’re illegal-but because they’re independent.

Let me ask you this: if you had a choice between a bank that monitors every dollar you move and a platform that lets you trade without asking questions-which one would you pick? The answer isn’t about ethics. It’s about autonomy.

So yes, use multiple exchanges. Yes, use DEXs. Yes, avoid KYC. Because the real crime isn’t trading crypto-it’s surrendering your financial freedom to a system that already stole your money through inflation, fees, and hidden taxes.

They want you afraid. Don’t give them that power.

Regulators are not the enemy. The real enemy is the illusion of safety that these platforms sell. People think they’re protecting themselves by avoiding KYC. In reality, they’re handing over their entire financial life to anonymous operators who can disappear with their funds at any moment. No recourse. No chargeback. No insurance.

And then they wonder why they lost everything.

It’s not about freedom. It’s about stupidity dressed up as rebellion.

Bro, if you’re using multiple exchanges to avoid restrictions, you’re not a hacker-you’re a sucker. Every single one of those ‘no-KYC’ platforms has a backdoor. Either they’re run by scammers, or they’re feeding data to regulators. You think you’re being sneaky? You’re the guy holding the sign that says ‘I’M DOING SOMETHING SUSPICIOUS’.

And don’t even get me started on DEXs. You think no one’s watching? Blockchain analytics firms have bots that track every swap. They don’t need your ID. They just need your wallet address. And guess what? Your address is already on a list because you used it on a sanctioned platform once.

Stop. Just stop.

Hey, I’ve helped over 200 people move crypto safely across borders. Most of them were just trying to avoid long bank delays, not evade sanctions. Here’s the truth: regulated exchanges are slow, expensive, and often block transfers from certain countries. That’s why people turn to alternatives.

But I get it-some of those alternatives are sketchy. So here’s what I tell everyone: if you’re going to use a non-KYC platform, use it once. Withdraw immediately to a verified wallet on a regulated exchange. Don’t leave funds there. Don’t trade there. Just use it as a bridge.

And always, always check the wallet history before sending. Use Etherscan or Bitcoin Explorer. If the previous 10 transactions are from known sanctioned addresses? Walk away.

It’s not about paranoia. It’s about hygiene.

THIS IS A PSYOP. 🤯

Regulators aren’t trying to stop crime-they’re trying to kill crypto. They know decentralized systems can’t be controlled. So they invented the ‘no KYC = illegal’ narrative to scare people into using banks. That’s why they’re targeting Grinex and Garantex-they’re not criminals, they’re threats.

And don’t fall for the blockchain analytics BS. They can’t trace everything. They just trace what they want you to see. The real money moves through private mixers, privacy coins, and onion networks. But you’ll never hear about those because the media only reports the ‘bad guys’ they catch.

Wake up. This isn’t about compliance. It’s about control. 🚨

I used to think using multiple exchanges was smart. Then I got locked out of my account on a nested platform. No customer service. No email replies. Just silence. I lost $12k. I didn’t even know they were holding my private keys. I thought I was ‘in control’. I wasn’t. I was a pawn.

Now I use one exchange. KYC. Full identity. I pay the fees. I accept the delays. Because I value my money more than I value the illusion of freedom.

Just… don’t be me.

The article is accurate. The data is solid. The regulatory framework is clear. Yet, the comments reveal a fundamental disconnect: many users still view crypto as a lawless space. This is not a technical issue. It is a behavioral one. The solution is not more regulation. It is better education. And yet, education is being drowned out by misinformation, YouTube influencers, and memes.

One cannot outsmart systemic risk through ignorance. The outcome is inevitable. And it is not pretty.

I used to trade on 5 exchanges. Now I use one. The difference? I sleep better. I don’t worry about frozen funds or being dragged into an investigation. I don’t need to know how every platform works. I just need to know that mine is licensed.

It’s not sexy. It’s not cool. But it’s safe.

And that’s enough.

There’s a quiet irony here. The same people who scream about ‘financial freedom’ are the ones willingly surrendering their data to unregulated platforms that don’t even have a CEO. You want autonomy? Then take responsibility. Own your wallet. Use your own node. Don’t trust a middleman who promises ‘no KYC’ while collecting your IP, device ID, and transaction logs.

True decentralization isn’t about avoiding regulators. It’s about removing intermediaries entirely.

Most of you aren’t decentralized. You’re just unregulated. And that’s not freedom. It’s vulnerability.

The legal and financial consequences of using non-compliant exchanges are not hypothetical. They are documented. They are enforced. They are escalating. The U.S. Department of Justice has prosecuted individuals for using DEXs to launder funds from darknet markets. The fines are not $500. They are $2.7 million. The prison sentences are not ‘maybe’. They are 12 years.

And yet, here we are. People still believe they’re ‘too small to matter’. They’re not. They’re the first domino. And regulators are trained to knock them down.

There is no such thing as a ‘harmless’ transaction on a sanctioned platform. There is only risk. And risk, in this context, is not an option.