When you provide liquidity to a decentralized exchange like Uniswap or Curve, you’re not just earning trading fees-you’re also taking on a hidden risk called impermanent loss. It’s not a glitch. It’s math. And if you don’t understand it, you could be losing money even when the price of your tokens goes up.

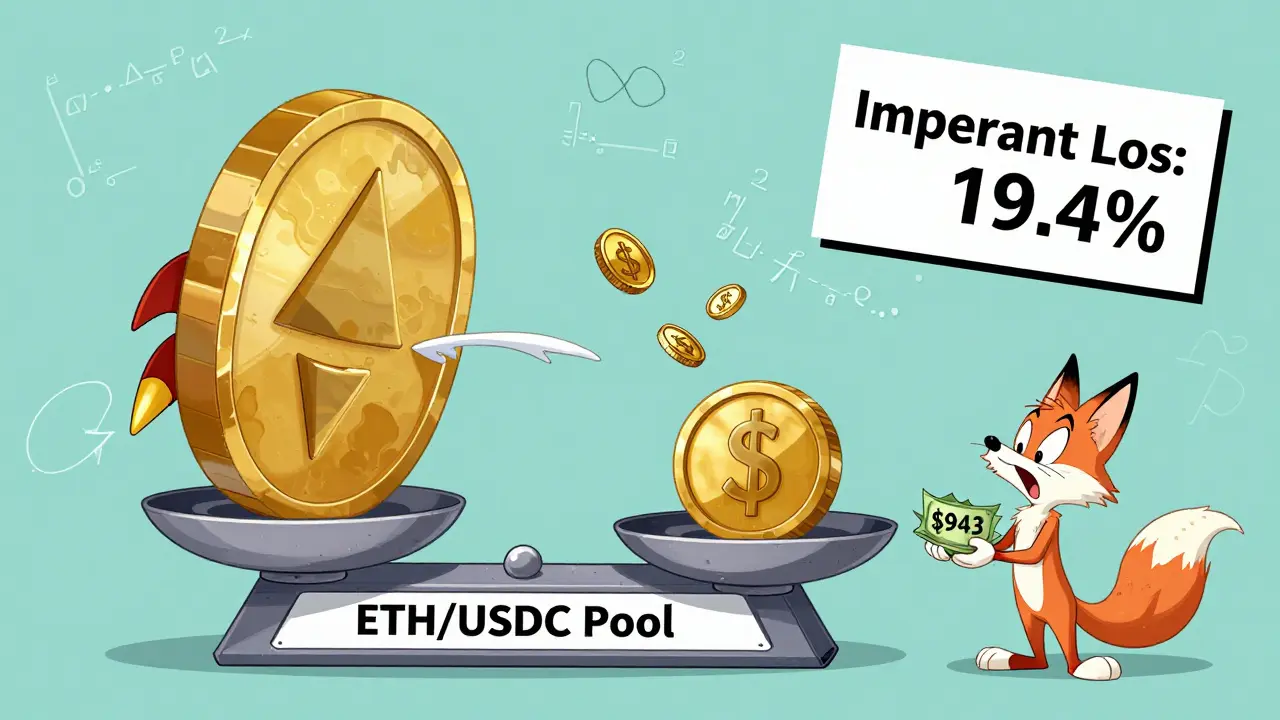

Imagine you put in $1,000 worth of ETH and USDC into a 50/50 liquidity pool. A week later, ETH doubles in price. You might think you’re up 100%. But when you check your position, you only see $943 in value. Where did the rest go? That’s impermanent loss. It happens because automated market makers (AMMs) rebalance your pool to match market prices. Arbitrage traders profit from the imbalance, and you’re left with more of the cheaper asset and less of the one that rose.

Why Impermanent Loss Happens

Impermanent loss isn’t about price movement alone. It’s about how much and how fast prices change relative to each other. In a standard 50/50 pool, the formula for impermanent loss is simple: 2√d / (1 + d) - 1, where d is the price ratio change. For example:

- 5% price change → 0.23% loss

- 20% price change → 2.0% loss

- 50% price change → 5.7% loss

- 100% price change (2x) → 19.4% loss

- 300% price change (4x) → 41.4% loss

This isn’t theoretical. In 2024, a popular ETH/USDC pool on Uniswap v3 saw over 60% of liquidity providers experience impermanent loss greater than 10% during a single volatile month. The loss is called "impermanent" because if prices return to their original ratio, the loss disappears. But in crypto, prices rarely go back. That’s why hedging isn’t optional-it’s survival.

Seven Ways to Hedge Against Impermanent Loss

There’s no one-size-fits-all solution. But here are the most effective methods used by top liquidity providers in 2025.

1. Use Stablecoin Pairs

The safest bet? Stick to pairs like USDC/USDT, DAI/USDC, or FRAX/USDC. These tokens are pegged to the dollar. Their price divergence is usually under 0.5% daily. That means impermanent loss is near zero. In 2025, liquidity providers on Curve Finance using USDC/USDT pairs reported average annual returns of 12% from fees alone-with impermanent loss averaging just 0.3%. No math. No stress. Just steady income.

2. Direct Hedging with Spot Trading

If you’re holding ETH/USDC liquidity, you can short ETH on a centralized exchange like Kraken or Coinbase. Every time ETH drops, your short position gains value and offsets the loss in your pool. This requires active monitoring. You need to track the price ratio daily and adjust your hedge. But it works. One user on Reddit reported offsetting 87% of impermanent loss over six months using this method. The catch? You pay trading fees and need enough capital to cover margin requirements.

3. Maximize Yield Farming Rewards

Many pools offer extra rewards in governance tokens. A pool like WETH/USDT on Uniswap might pay 50% APY in UNI tokens. If your impermanent loss is 15%, but your rewards are worth 20%, you’re still ahead. In 2025, some high-activity pools on Arbitrum offered over 100% APY in token incentives. But beware: if the reward token crashes, you’re left with a loss and a worthless asset. Use this as a buffer, not a solution.

4. Use Impermanent Loss Protection Protocols

Bancor pioneered this. If you lock liquidity for 100 days, they’ll fully reimburse you for any impermanent loss. Other protocols like SushiSwap and Balancer now offer similar features with tiered protection: 20% after 30 days, 50% after 60, 100% after 100. This is ideal for passive holders. You don’t need to do anything. Just stake and wait. The catch? Your funds are locked. You can’t withdraw early without losing protection.

5. Diversify Across Multiple Pools

Don’t put all your liquidity in one pair. Spread it across five to ten pools: ETH/USDC, SOL/USDC, AVAX/USDT, WBTC/DAI, and even a few stablecoin pairs. This reduces your exposure to any single asset’s volatility. Portfolio theory applies here: the more uncorrelated assets you include, the lower your overall risk. A 2025 study from the Simons Foundation showed that diversified liquidity providers had 40% less average impermanent loss than those focused on one pair.

6. Options-Based Hedging

This is for advanced users. Buy put options on the volatile asset in your pool. For example, if you’re in ETH/USDC, buy ETH puts. If ETH crashes, your puts pay out and cover your pool loss. Some platforms like Lyra and DerivaDAO now offer crypto-native options with low gas fees. But options pricing is complex. You need to understand delta, gamma, and vega. Most retail traders lose money on options. Only use this if you’ve traded options before.

7. Automated Range Management

Uniswap v3 let you set custom price ranges. But manually adjusting them is a full-time job. New protocols like ERC-7702 is a smart contract standard that enables account abstraction are changing that. Protocols like Range Protocol and DeFiHedge now auto-adjust your liquidity range based on real-time volatility. If ETH moves 10%, the smart contract shifts your range to stay in the fee zone. This reduces impermanent loss by up to 70% compared to static positions. It’s the future-and it’s live now.

What Works Best for Different Users

Not everyone has the same goals, time, or capital. Here’s who should use what:

| User Type | Best Strategy | Time Required | Capital Needed |

|---|---|---|---|

| Beginner | Stablecoin pairs (USDC/USDT) | 30 minutes to set up | $500+ |

| Intermediate | Yield farming + diversification | 2 hours/week | $2,000+ |

| Advanced | Automated range management | 1 hour/week | $10,000+ |

| Professional | Options + direct hedging | 5+ hours/week | $50,000+ |

Most retail users start with stablecoin pairs. They’re boring. But they’re the only way to guarantee you won’t lose money. The rest? That’s where the real money is made-for those who know how to play.

Why Most People Fail at Hedging

Two mistakes keep killing returns:

- Ignoring gas fees. Manual hedging on Ethereum costs $15-$30 per trade. If you’re only staking $2,000, you’ll burn through your profits before you break even. Always use Layer 2 networks like Arbitrum or Base. Gas is under $0.10.

- Chasing high APY. A pool offering 150% APY in a new meme coin is a trap. That coin might crash 90% in a week. Your rewards vanish. Your impermanent loss stays. You end up with less than you started.

Successful hedging isn’t about winning big. It’s about losing less. The goal isn’t to make 100%. It’s to make 12% without losing 15%.

What’s Coming Next

By late 2026, most major AMMs will have built-in hedging. Uniswap v4 is expected to launch with native automated range adjustment. Machine learning models will predict volatility spikes and adjust liquidity ranges before prices move. Cross-chain hedging will let you protect ETH on Ethereum while holding SOL on Solana-all in one contract.

Right now, you have a choice: stay passive and risk losing money, or learn to hedge and turn liquidity provision into a reliable income stream. The tools are here. The math is clear. The only thing left is to act.

Is impermanent loss real, or just a myth?

It’s real. Every time the price of two tokens in a liquidity pool changes relative to each other, the AMM rebalances your holdings. If one token rises sharply, you end up with more of the cheaper token and less of the one that went up. The math proves this loss is predictable and measurable. It’s not a bug-it’s how AMMs work.

Can you eliminate impermanent loss completely?

Not completely, but you can reduce it to near zero. Using stablecoin pairs like USDC/USDT cuts impermanent loss to under 0.5% annually. Some protocols offer full reimbursement after 100 days. Automated systems can cut losses by 70% or more. But if you’re using volatile pairs like ETH/BTC, some loss is inevitable.

Do I need to be a crypto expert to hedge?

No. Beginners can start with stablecoin pairs on Curve or Uniswap-no expertise needed. Intermediate users can use yield farming and diversification. Advanced users can try automated range management. Only options-based hedging requires deep knowledge. You don’t need to be a trader to protect your capital.

Is it worth hedging if I only have $1,000?

Yes, but only with stablecoin pairs. Manual hedging or options trading costs too much in gas fees for small amounts. With $1,000, your best move is to stake USDC/USDT on a low-fee chain like Base or Arbitrum. You’ll earn 10-12% APY from fees and avoid almost all impermanent loss. That’s better than 90% of DeFi users.

What’s the difference between impermanent loss and permanent loss?

Impermanent loss is temporary-it disappears if prices return to their original ratio. Permanent loss happens when you sell your position at a lower value than you deposited. For example, if ETH crashes 50% and you withdraw, you’ve lost money. That’s permanent. Impermanent loss is a math problem. Permanent loss is a decision problem.

Should I avoid volatile pairs like ETH/BTC?

If you’re not hedging, yes. ETH/BTC pools have high trading fees, but they also have high impermanent loss. A 2x move in ETH relative to BTC can cause over 30% loss. Only use these if you’re actively hedging with automated tools or options. For most people, stick to stablecoin pairs or single-asset pools.

Impermanent loss isn't a bug-it's a feature of capitalism disguised as decentralized finance. The entire system is designed to transfer wealth from the uninformed to the algorithmically sophisticated. You think you're earning fees? You're subsidizing arbitrage bots with your capital. The real yield isn't in liquidity pools-it's in knowing which pools to avoid.

Stablecoin pairs work. Simple. No drama. No math. Just steady returns.

Oh wow, a 12% APY on USDC/USDT? How thrilling. I almost cried. Meanwhile, I’m over here staking ETH on a Layer 3 chain with 400% APY in a token that hasn’t even launched yet. At least my losses are *artistic*.

Most people don’t understand that impermanent loss is just a symptom of volatility. The real issue is chasing yield without understanding risk. Stick to stable pairs. Stay alive.

I’ve been in DeFi since 2021 and I still get nervous every time I add liquidity. I remember one time I put in $5k in WBTC/ETH and watched it drop 38% over three weeks because BTC dipped while ETH surged. I almost quit crypto entirely. But then I started using automated range management on Uniswap v3 and now I sleep better. It’s not perfect, but it’s the closest thing to peace of mind I’ve found in this space. I still check my positions every morning like a parent checking on a sleeping child. It’s weird, I know. But I’ve learned that in crypto, emotional discipline beats clever strategy every time.

yo u think u r smart with all this math? u just got rekt by a bot that ran a flash loan on ur pool. 100% loss? nope. 100% ignorance. why u even use eth? go to solana. gas is 0.000001. u r so 2020.

It’s funny how we treat impermanent loss like some cosmic injustice. The market doesn’t care if you’re ‘up 100%’ in your head. It only cares about what’s in your wallet. We’re not investors-we’re accountants with delusions of grandeur.

In India, many beginners start with stablecoin pairs on CoinSwitch. Low gas, low risk. Once you understand how AMMs work, you can move to diversified pools. Patience > hype.

They say ‘stick to stablecoins’-but who’s behind these stablecoins? The same banks that crashed the system in 2008. USDC? Backed by BlackRock. This whole thing is a trap. You think you’re decentralized? You’re just paying fees to the same elite. The real hedge is cash. Gold. A shotgun. And a bunker.

This is actually one of the clearest breakdowns I’ve seen. I’ve been doing yield farming for a while and I didn’t realize how much I was losing until I ran the numbers. I switched to USDC/USDT on Base and my returns went from ‘meh’ to ‘actually worth my time.’ Also, gas fees on Ethereum were killing me-switching to Layer 2 was the best move I made this year. Keep sharing stuff like this. It helps more than you know.

Yield farming is a Ponzi if the tokenomics are flawed. You think 100% APY is sustainable? The token is a meme. The pool is a graveyard. The only thing that matters is liquidity depth and protocol security. All this hedging is just theater. The real edge is in on-chain analytics and MEV detection. You’re all playing checkers while the whales play chess.

I tried the Bancor protection thing. Locked up my ETH for 100 days. Then I needed cash for rent. Had to wait. Lost 3 weeks of interest. Then the protocol had a minor bug and my transaction got stuck. Took 4 days to fix. I’m never doing that again. Just give me a simple interface. Not a PhD thesis.

As someone who’s been in crypto since 2017, I’ve seen every trend come and go. The best advice? Don’t chase yield. Chase stability. Use stablecoin pairs. Use Layer 2. Use automation. Don’t overcomplicate it. The market rewards patience, not cleverness.

Thank you for writing this. I was about to put my savings into a 200% APY pool on a new chain. I almost lost everything. Your breakdown saved me. I switched to USDC/USDT on Arbitrum last week. Got 11.8% APY. No stress. No sleepless nights. Just peace. You’re doing good work.