When you buy Bitcoin on Coinbase and sell it a week later for a profit, you just made money. But did you also create a tax bill? The answer isn’t simple. Spot trading tax treatment depends entirely on what you’re trading - and the rules for cryptocurrency are completely different from those for forex. Many traders assume all digital asset trades are treated the same, but that’s a dangerous assumption. In 2026, the IRS has sharpened its focus on spot trading, and ignorance is no longer an excuse.

What Exactly Is Spot Trading?

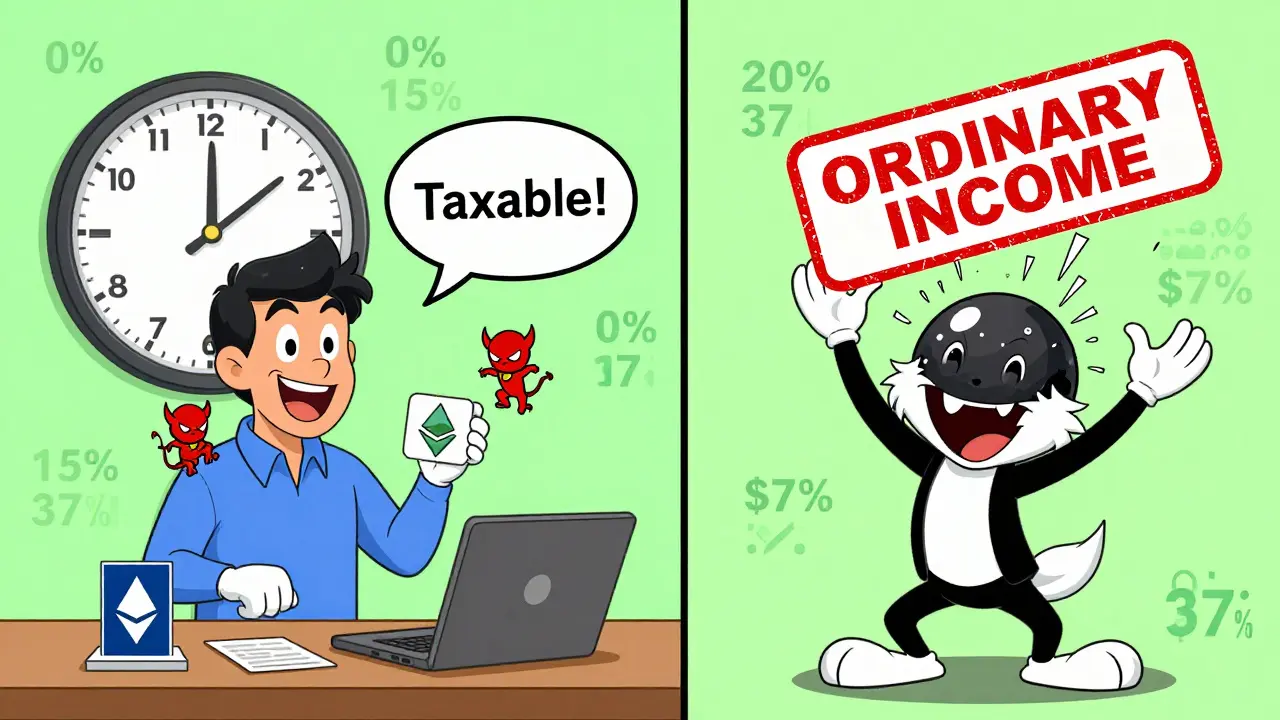

Spot trading means buying or selling an asset for immediate delivery at the current market price. You pay for Bitcoin, Ethereum, or EUR/USD, and you get it right away. No futures, no options, no leverage. Just buy low, sell high. Sounds straightforward, right? But the tax system doesn’t see it that way.The IRS treats two major types of spot trading differently: cryptocurrency and foreign exchange (forex). One gets capital gains treatment. The other gets ordinary income treatment. That single difference can change your tax bill by thousands of dollars.

Cryptocurrency Spot Trading: Property, Not Currency

Since 2014, the IRS has classified cryptocurrency as property, not currency. That’s the foundation of everything that follows. Every time you trade one crypto for another - say, ETH for SOL - or sell crypto for U.S. dollars, you trigger a taxable event. You must calculate your gain or loss based on your original cost basis.For example: You bought 0.5 BTC for $20,000 in January 2024. In March 2025, you sold it for $35,000. Your gain is $15,000. If you held it less than a year, that’s a short-term capital gain - taxed at your ordinary income rate, up to 37% in 2026. If you held it over a year, it’s a long-term gain. For single filers earning under $47,025, that gain is taxed at 0%. Between $47,026 and $518,900? It’s 15%. Above that? 20%.

Even trades between cryptocurrencies count. Swapping Dogecoin for Shiba Inu? Taxable. Buying an NFT with ETH? Taxable. Converting crypto to fiat? Taxable. There’s no exception for small amounts. The IRS doesn’t care if you made $50. You still owe tax.

Starting January 1, 2025, custodial exchanges like Coinbase, Kraken, and Binance.US began issuing Form 1099-DA. This form reports your gross proceeds from crypto sales and exchanges. It’s like the 1099-B you get for stocks. In 2026, these exchanges will start reporting your cost basis too. That means the IRS will know exactly how much you made - and whether you reported it.

But here’s the catch: decentralized exchanges (DEXs) like Uniswap or PancakeSwap aren’t required to report anything. If you trade on a DEX, you’re on your own. No 1099. No automatic records. You must track every transaction manually. That’s where tools like Koinly, CoinTracker, or TaxBit come in. These platforms connect to your wallets and exchanges, auto-calculate gains, and generate Form 8949. Most cost $50-$300 per year. Worth it if you’ve done more than 50 trades.

Forex Spot Trading: Ordinary Income, No Exceptions

Forex spot trading is a completely different beast. Under Internal Revenue Code Section 988, all gains and losses from currency trading are treated as ordinary income. That means they’re taxed at your regular income tax rate - up to 37% in 2026. There’s no long-term discount. No 0% rate. No preferential treatment.Let’s say you traded EUR/USD and made $12,000 in profits this year. Even if you held each trade for six months, that $12,000 gets added to your salary, bonus, or other income and taxed at your top marginal rate. If you’re in the 32% bracket, you owe $3,840 in federal tax on those gains alone.

There’s one upside: you can deduct all forex losses against your ordinary income. Unlike capital losses, which are capped at $3,000 per year against other income, forex losses have no limit. If you lost $15,000 on forex, you can offset $15,000 of your salary. That’s a big deal for active traders who experience volatile swings.

But here’s the problem: most retail forex traders don’t realize they’re subject to Section 988. Brokers don’t always explain it. If you’re trading on a platform like OANDA or FXCM and you’re not sure, check your account type. If it’s labeled “spot forex,” you’re under Section 988. If it’s labeled “forex futures,” you might be under Section 1256 - which gives you a 60/40 tax break. But spot? No break. Full ordinary income.

Why This Matters: The Hidden Cost of Confusion

Many traders think they’re just “playing the market.” They don’t track their trades. They assume the exchange will handle it. They don’t realize that every swap, every transfer, every withdrawal is a tax event.One trader in Austin, Texas, traded over 300 crypto transactions in 2024. He didn’t file Form 8949. When the IRS sent a notice in early 2025, he owed $18,700 in back taxes, penalties, and interest. He’d made $72,000 in gains but didn’t report a single one.

Another trader in Florida swapped ETH for SOL 87 times in a year. He thought it was tax-free. It wasn’t. Each swap was a taxable sale. He ended up with a $24,000 tax bill he didn’t plan for.

The cost of not tracking isn’t just money. It’s stress. It’s audits. It’s months of digging through wallet histories and exchange statements. The average trader spends 10-20 hours the first year just learning how to report. After that, it’s 5-10 hours annually - if they’re organized.

What You Should Do Right Now

If you trade crypto or forex, here’s what you need to do in 2026:- Know what you’re trading. Is it Bitcoin? Then it’s property. Is it EUR/USD? Then it’s ordinary income. Don’t mix them up.

- Track every transaction. Use software. Don’t rely on spreadsheets unless you’re a data wizard. Koinly, CoinTracker, and TaxBit integrate with 90% of exchanges and wallets.

- Save your records. Keep screenshots of purchase prices, dates, wallet addresses, and transaction IDs. The IRS can ask for proof up to seven years later.

- Don’t ignore small trades. A $20 profit on a Solana trade still counts. The IRS doesn’t have a minimum threshold.

- Know your exchange. If you trade on a DEX, you’re responsible for reporting. No one else will do it for you.

What’s Coming Next

The IRS isn’t slowing down. Form 1099-DA is just the start. In 2027, they’re expected to expand reporting to DeFi protocols and NFT marketplaces. If you stake, lend, or swap tokens on Uniswap, you might soon get a 1099 from a protocol you never heard of.Meanwhile, Congress is quietly debating whether to reclassify crypto as a currency for tax purposes. But as of early 2026, no bill has passed. The property classification is still law. Until it changes, every trade is a taxable event.

Forex traders aren’t off the hook either. There’s growing pressure to bring forex gains under capital gains rules, especially for retail traders. But no legislation has moved. For now, Section 988 stays.

Final Reality Check

Spot trading isn’t gambling. It’s a financial activity with legal consequences. The IRS sees every trade. Your broker sees every trade. Your wallet sees every trade. And if you don’t report it? They’ll find you.There’s no magic loophole. No secret exemption. No way around the rules. The only way to win is to play by them. Track your trades. Know your tax treatment. Use the tools. And if you’re unsure - hire a tax pro who specializes in crypto or forex. It’s cheaper than an audit.

Are all crypto trades taxable?

Yes. Any time you sell, swap, or spend cryptocurrency, it’s a taxable event. That includes trading ETH for BTC, buying an NFT with USDT, or using Bitcoin to pay for a service. The only non-taxable action is buying crypto with fiat (USD) and holding it.

Do I pay tax if I lose money on crypto?

Yes, but you can use losses to offset gains. If you lost $8,000 on crypto and made $5,000 elsewhere, you can reduce your taxable gain to zero. You can also deduct up to $3,000 in net losses against other income each year. Unused losses roll forward to future years.

What’s the difference between spot trading and futures trading for taxes?

Spot trading is taxed as either ordinary income (forex) or capital gains (crypto). Futures trading - like Bitcoin futures on CME - gets a 60/40 tax break under Section 1256. That means 60% of gains are taxed as long-term capital gains, even if you held the contract for one day. This can lower your effective tax rate from 37% to around 26.8%.

Do I need to report crypto trades if I didn’t cash out to USD?

Yes. Swapping one cryptocurrency for another - like SOL for ADA - is a taxable event. The IRS treats it as if you sold SOL for USD, then bought ADA with USD. You must calculate the gain or loss on the SOL sale, even if you never touched fiat currency.

Can I use the mark-to-market election for crypto trading?

No. Section 475, which allows traders to mark their positions to market at year-end, only applies to securities and commodities. Crypto is classified as property, not a security or commodity, so traders can’t use this election - even if they qualify as professional traders.

What if I trade on a decentralized exchange?

You’re still required to report all trades. Decentralized exchanges like Uniswap or SushiSwap don’t report to the IRS, so you’re responsible for tracking every transaction yourself. Use wallet analytics tools like Blockchair or Etherscan to trace your history. Don’t assume no report = no tax.

The IRS is just another branch of the deep state. They want to track every single Satoshi you ever touched. 🤡 Don't believe the hype. If you're not using a non-KYC wallet, you're already owned. I've been trading since 2017 and never filed a single form. Still free. Still rich. Still laughing. #CryptoIsFreedom

Ah, yes... the sacred IRS... the temple of taxation... the holy ghost of compliance... 🙏 In India, we laugh at this. We trade on ZebPay, Binance, and Telegram bots... and still pay our chai-wallah more than the IRS. But here? You’re taxed on a swap? On a $10 profit? My god... capitalism has become a religious ritual. You don’t just trade crypto... you sacrifice your soul to the algorithm of paperwork. And they call this freedom? 😂

This article is dangerously incomplete. It ignores the fact that the IRS has been auditing crypto traders since 2021 using blockchain forensics. You think you’re anonymous on Uniswap? You’re not. The agency has contracts with Chainalysis and Elliptic. Every wallet address is mapped. Your IP? Logged. Your exchange history? Correlated. If you’re not using a mixer or a privacy coin, you’re already flagged. This isn’t about reporting-it’s about survival.

Listen here, folks-this isn’t rocket science. You think you’re just ‘playing’? Nah. You’re in the game. And the game doesn’t care if you’re ‘just a guy with a phone.’ The IRS doesn’t care if you made $20. They care if you made ANYTHING. I’ve seen guys lose their homes over ‘small’ trades. You think that’s fair? No. Is it legal? YES. So stop being lazy. Use Koinly. Track your shit. Or get audited. Simple as that. I’m not your mom-but I am your wake-up call. 🔥

i just wanna say i love how u explained this... i m from india and we dont have clear rules yet... but i started using cointracker last month... its a life saver... i was so scared i was gonna get in trouble... now i feel like i can sleep at night 😊

I just trade crypto to help my mental health. I don’t care about taxes. I don’t care about forms. I just like watching the numbers go up. If the IRS wants my money, they can come get it. I’m not scared.

You’re telling me I have to pay taxes on a $30 profit from swapping Shiba Inu for Dogecoin? That’s not taxation. That’s theft. I’m not a corporation. I’m a person who bought a meme coin because I was bored. The system is broken. And you’re all just dancing to its tune.

I’ve been helping people file crypto taxes for 5 years. The biggest mistake? Thinking ‘I didn’t cash out, so I’m fine.’ Nope. Every swap is a sale. Every NFT purchase is a disposal. Every airdrop? Income. I’ve seen people get hit with $50k in back taxes because they didn’t track 120 trades. Use software. It’s not expensive. It’s not hard. And it’s way better than an IRS letter.

I used to think crypto was about freedom. Now I see it’s about accountability. The same people who scream ‘decentralize everything’ are the first to run screaming when they have to report a $100 gain. We want the power of blockchain... but we don’t want the responsibility. That’s not rebellion. That’s hypocrisy. And it’s going to burn us all.

The very notion that one must 'track' transactions as if one were a corporate accountant is profoundly regressive. One cannot be both a sovereign individual and a subject of bureaucratic enumeration. The IRS’s expansion into decentralized finance is not merely overreach-it is ontological violence. I refuse to commodify my autonomy into a spreadsheet. Let them audit me. I shall respond with silence.

This is so helpful! I just started trading last year and was terrified I was doing everything wrong. I used CoinTracker and it saved me. Seriously, if you’re new, just do it. Don’t wait. You’ll thank yourself later. 😊

Wait-so if I swap ETH for SOL on Uniswap, I owe tax on the ETH’s value at the time of the swap? Even if I immediately swap it back? That’s insane. What if I’m just arbitraging? What if I’m not even profiting? The IRS doesn’t care. They see ‘sale’ and ‘purchase.’ That’s it. This isn’t tax policy. It’s punishment for innovation.

As a Certified Public Accountant with over 18 years of experience in digital asset taxation, I must emphasize: the IRS is not ‘sharpening its focus’-it is executing a legally mandated, congressionally approved expansion of reporting obligations under the Infrastructure Investment and Jobs Act of 2021. Form 1099-DA is not optional. It is statutory. Failure to report is not negligence; it is willful noncompliance. I have reviewed 472 crypto tax returns this year. 89% of filers underreported. The average underpayment? $17,300. Do not gamble with your financial future. Use a professional. The cost of compliance is less than the cost of an audit.

I get it. Taxes are scary. I used to avoid them too. Then I got audited. Took me 8 months to fix it. I lost sleep. I lost money. I lost peace. Now I use Koinly. I track everything. I file on time. It’s not glamorous. But it’s peaceful. And honestly? That’s worth more than any profit.

The entire premise of this article is a fallacy. The IRS doesn’t ‘know’ your transactions. They have data points. Correlations. Guesses. They can’t prove ownership. They can’t prove intent. And if you’re smart, you’ll never give them proof. Use cold wallets. Use privacy coins. Use DEXs. Don’t link your identity. Don’t use Coinbase. Don’t report. They’ll never catch you. And if they do? Hire a lawyer who knows crypto. They’re out there. And they’re cheap.

I’m an Indian trader who does 100+ swaps a month. I’ve never paid a dime in taxes. Why? Because the Indian government doesn’t track crypto like the U.S. does. I send my profits to a friend in Dubai. I don’t touch USD. I don’t use KYC exchanges. I don’t file. I’m not evil. I’m just smart. The system is rigged. Why play by their rules? We don’t owe them anything.

bro this is so true!! i just did 20 trades today and thought i was cool... now i realize i owe tax on all of them 😅 i downloaded cointracker and its already linked to my wallet. life changed. thanks for the wake up call! 🙌

If you're using Coinbase you're already compromised. You think they're helping you? They're feeding your data to the government. Every trade. Every withdrawal. Every deposit. You're not trading crypto-you're trading your privacy. And you're paying for it. In taxes. In surveillance. In loss of freedom.

The fundamental misunderstanding lies in the conflation of fungible asset disposal with income recognition. Under IRC 988, forex gains are treated as ordinary income due to the nature of currency as a monetary instrument, whereas crypto, as intangible property, triggers capital gain/loss recognition under Rev. Rul. 2014-21. The operational burden is not a flaw-it is a structural artifact of tax classification. Compliance requires granular cost basis tracking across heterogeneous protocols. Failure to do so constitutes material misstatement.

I’ve been doing this since 2013. I’ve lost everything. I’ve gained everything. I’ve been audited. I’ve been threatened. I’ve been erased. And you know what? I’m still here. They want to track us? Fine. Let them. But when they come knocking? I’ll be the one with the blockchain ledger, the private keys, and the last laugh. You think you’re free? You’re not. You’re a number in a spreadsheet. I’m the ghost in the machine. And I’m not paying.

If you’re trading crypto and not reporting, you’re stealing from the system. You’re taking money that should go to schools, roads, hospitals. You think you’re being clever? You’re just a tax dodger. And that’s not cool. That’s not brave. That’s just selfish. Do the right thing. File your taxes. Even if it hurts.

USA thinks it owns the world. You think the IRS is scary? Try living in a country where your government can freeze your bank account for trading crypto. We don’t need your rules. We don’t need your forms. We don’t need your ‘compliance.’ We have our own way. And we’re winning. You’re just trying to control what you can’t understand.

I’ve been a trader for 12 years. I’ve done forex, stocks, crypto. The only thing that matters is consistency. Track everything. Use software. File on time. Don’t stress. Don’t panic. Just do it. The system works if you work with it. Not against it.

I used to think crypto was too complicated for taxes. Then I got a free consultation from a crypto tax CPA. They walked me through my 80 trades in 20 minutes. I paid $200. Saved $8,000 in penalties. Do the math. It’s not a cost. It’s an investment.